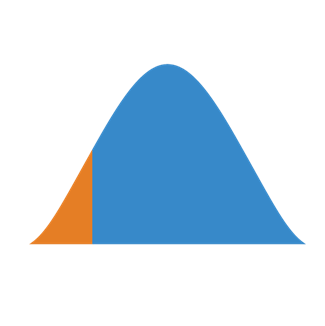

Our aim: to capture the perfect shape

We generate alpha by selecting right skewed return distributions with minimal left tail risk.

The aim of our process

Value strategies in Japan can be highly profitable. Returns are greatly skewed to the right with fat right tails. However, plain vanilla value investing in Japan comes with significant drawdowns. Macro events occur on a regular basis with liquidity and currency dislocation causing substantial draw downs. The defining characteristics of our value philosophy therefore focus on understanding risk and actively managing the left tail to ensure a comprehensive perspective and the full realization of the opportunity set.

Our process in three steps:

-

1 - Single Stock Selection

-

Limited universe – Is the business model understandable?

Limited universe – Is the business model understandable?

We have identified a distinct circle of competence and only expose risk capital to what we deem understandable. We shy away from pharma, regulated industries such as telecom and utilities and dislike short cycle business models such as technology and consumer electronics. We spent most of our time on fundamental bottom-up analysis in industrials, materials and consumer related business with high tangible assets.

Investment thesis – What is in the price?

Investment thesis – What is in the price?

We evaluate the business model and dissect financial statements in order to arrive at the intrinsic value considering various risk scenarios. Having exposure to a business model means having exposure to various likely future outcomes. Only one reality will occur and the closer we come to understanding future outcomes and the extend to which they are reflected in the share price, the greater our degree of success.

Corporate Governance

Corporate Governance

We identify companies where improvements in corporate governance are likely to benefit shareholders. We engage with management of companies to make those improvements happen.

-

2 - Portfolio Construction

-

Position sizes – What is the perceived versus expected risk?

In our opinion, risk is not volatility. Our bottom-up understanding of the business models enables us to understand the risk of permanent capital loss. Cheap stocks tend to carry less risk than perceived and investors in expensive stocks tend to be too negligent. We actively manage position sizes and impose maximum limits on single stocks.

Construct – How does the collection of single stock pay offs fit together?

Our portfolio is a collection of bottom-up stock picks with target prices and stop losses; a collection of single stock distributions. We measure concentration risk and dissect variance contribution accordingly. We want to minimize unintended bets and, taking correlation into account, optimize intended bets.

-

3 - Risk Management

-

Stop loss

Stop loss

Every trade has a stop loss and target price. These levels are determined using technical analysis as well as a fundamentally assigned intrinsic value.

Active Sizing

Active Sizing

We actively manage position size depending on risk/reward and alternative opportunities. Single stock high water mark alerts of 50bps and 100bps are combined with stop loss levels.

Macro Insight

Macro Insight

We systematically monitor macro factors to distinguish noise from signal and improve beta exposure and sector allocation, as well as single stock risk budgeting.